Based on the six topics of rationality, confidence, money, regulation, business and globalisation, these imaginary radio programmes provide a pretext for discovering 18 renowned economists who have greatly influenced the currents of economic thinking.

Choose your programme :

They are quoted in the programme, learn more about them :

© Collection BSI/CSI

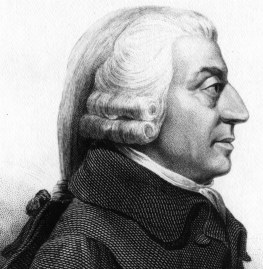

© Collection BSI/CSI Adam Smith

The Scottish philosopher and economist Adam Smith was born in 1723 in Kircalky (Scotland) and died in 1790 in Edinburgh. He is widely viewed as the father of political economics

At the age of 27, Smith was appointed to the Chair of Logic at the University of Glasgow and subsequently that of Moral Philosophy. In 1765, he spent a brief spell in France where he frequented economists such as Quesnay and Turgot. His principal work, "An Inquiry into the Nature and Causes of the Wealth of Nations" was published in London in 1776.

Smith demonstrated that the wealth of nations is born of the division of labour. A free trade thinker, he formulated the so-called "absolute advantage" law according to which all countries have an interest in specialising in productions which they achieve at the least cost and described the famous mechanism of the "invisible hand" which, in his view caused individual acts and the general interest to converge in a market economy.

© Archives UNIL/Université de Lausanne, Suisse

© Archives UNIL/Université de Lausanne, Suisse Léon Walras

The French economist Léon Walras was born in Évreux in 1834 and died in Clarens (Switzerland) in 1910.

After studying at the École des mines de Paris, he dabbled with careers as a publicist and art critic before embracing political economics like his father before him, Auguste. He worked on the "Journal des économistes" and published numerous writings. Walras passed the entrance exam to become professor at the University of Lausanne at the age of 36. He was one of the first economists to apply mathematics to the study of economic developments.

Walras was behind the theory of general equilibrium of prices and exchanges in a regime of perfect competition. He promoted the idea that under certain conditions the confrontation between supply and demand generated a price system which caused all markets to achieve equilibrium.

© Collection Bettmann/CORBIS

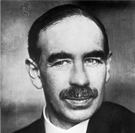

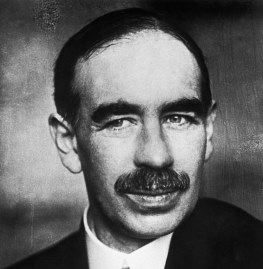

© Collection Bettmann/CORBIS John Maynard Keynes

The British economist John M. Keynes was born in Cambridge (United Kingdom) in 1883 and died in Firle, Sussex (United Kingdom) in 1946. He has had a considerable influence over western economic policies through to the present day.

A university professor trained in Cambridge, Keynes was a senior treasury official during the First World War. He became famous in 1936 with the publication of his book "The General Theory of Employment, Interest and Money" and was appointed financial adviser to the Crown. He headed the British delegation to the Bretton Woods Conference in 1944.

Reasoning in terms of macroeconomics, Keynes rejected the notion that a market economy is able to self regulate in order to achieve full employment and recommended intervention by the state in times of economic turmoil so as to shore up demand and stimulate investment.

© University of Chicago, USA/Licence Creative Commons

© University of Chicago, USA/Licence Creative Commons Robert Lucas

Born in 1937 in Yakima (US state of Washington), Robert Lucas is an American economist and free-market thinker who represents the new classical school.

After studying history and economics at the University of Chicago, he took a teaching post at the Carnegie Institute of Technology in Pittsburgh, then Chicago. Influenced by the monetarist ideas of Friedman and Samuelson, Lucas was awarded the Nobel Prize for Economics in 1995 for his work on rational anticipations.

His theory affirms that economic agents anticipate the future – and adapt their behaviour as a consequence, at which stage, the interventionist policies of governments become pointless.